Where is the housing market headed? The U.S. housing market could be in a recovery that is showing signs of slowing. Or perhaps it is recovering too quickly and another bubble is forming which is on its way to bursting.

The true nature and the direction of the housing market recovery may depend entirely on one's vantage point. Increasingly, we are beginning to see that what looks like a recovery is actually concentrated to few markets and the reality is that a number of cities and neighborhoods are limping along and many households are still wounded from the housing crash.

In an environment where the recovery can vary so dramatically from state to state, city to city, and neighborhood to neighborhood, there's a real need for information that can help us better understand the factors contributing to the relative strength and weakness of different housing markets. This type of information can give us a clue as to the nature of the recovery - and help us prepare for what's next.

In the last few months, IHS has released two separate reports that add to the understanding of the current health of both the local and national housing markets and what may lie ahead.

The most current release of the IHS Cook County House Price Index found recent strong price gains are being led by activity in a small set of neighborhoods, and most areas in the County are recovering more slowly. The second report, a Research Brief on the potential impact of rising interest rates on housing turnover, identified a potential roadblock when looking down the road at long-term nationwide recovery

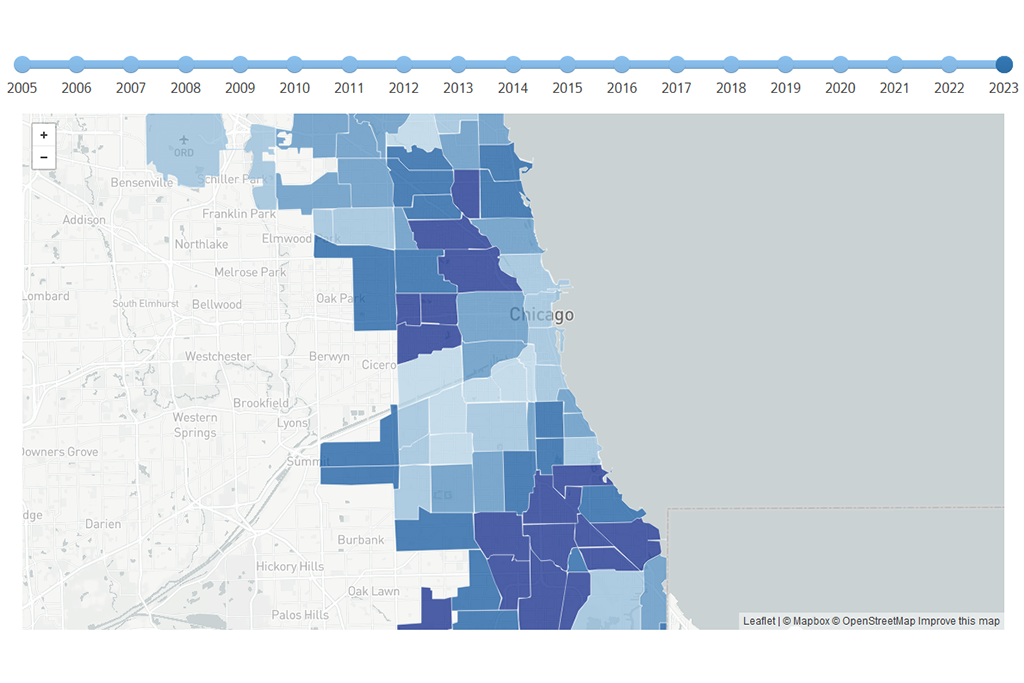

Taking a closer look at an uneven housing market recovery in Cook County

Our most recent release of the quarterly Cook County House Price Index found that home prices for single family properties in Cook County ended 2013 up 15.1 percent from the previous year - their greatest year-over-year increase in the sixteen years measured by the Index.

Though this certainly sounds like a market in recovery, the Chicago Tribune's coverage of the Index highlighted that caveats abound. Despite these increases, County prices are still only at 2002 levels, and a slowing of quarter-to-quarter price increases may indicate cooling off in a market that still has a long way to go.

While nearly every submarket in the County had annual price gains, these increases varied dramatically by neighborhood. For example, a small group of neighborhoods experienced sharp house price rebounds of over 20 percent, while at the other end of the spectrum, a group of neighborhoods continue to struggle seeing flat or even declining house prices. In spite of these recent gains, most submarkets are still at price levels seen in the early 2000s

In fact, the submarkets that have emerged from the housing crisis with the strongest and most stable house prices are the same neighborhoods that saw the least amount of price decline during the crash. So while these areas didn’t see the biggest increases in 2013, they are still farther along the road to full recovery than other submarkets in Chicago.

Examining a potential obstacle to full recovery

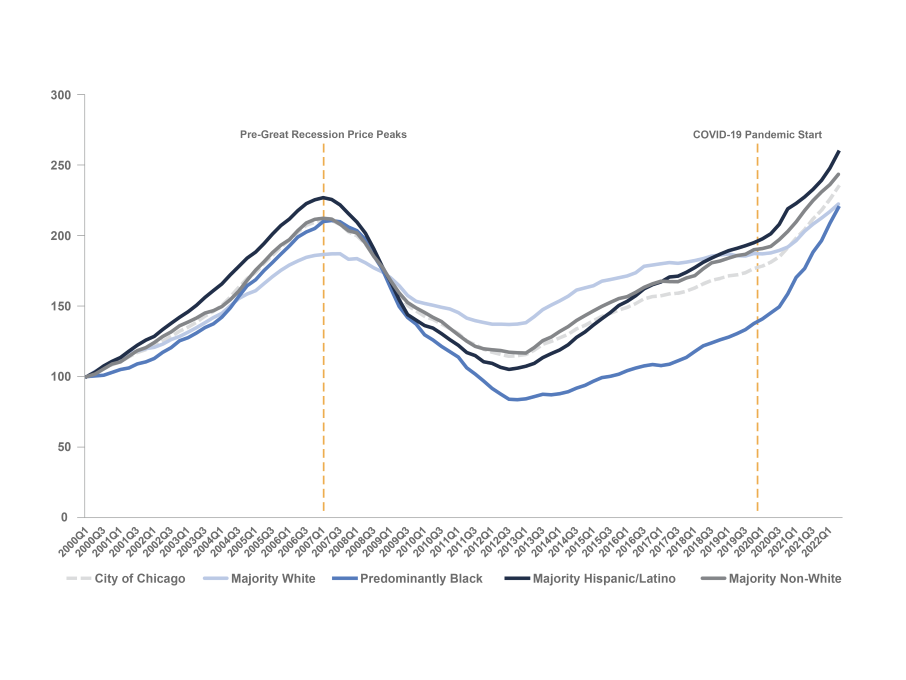

While IHS's Cook County House Price Index highlighted variations in neighborhood price trends, a recently released Research Brief used data from Cook County to examine a possible barrier to nationwide housing market recovery and how this barrier might have the largest impact on neighborhoods with strong housing markets - the same markets that have buoyed house prices in Cook County in recent years.

“The Impact of Lock-In Effects on Housing Turnover and Implications for a Housing Recovery” examines the potential impact of rising long-term interest rates on housing turnover going forward. The Brief’s central thesis is that the recent period of historically low long-term interest rates may lead to depressed housing turnover because the millions of owners who purchased or refinanced at those historically low rates will be reluctant to give them up as interest rates rise.

A recent New York Times piece examined this issue and looked at additional data that pointed to owners choosing to rent instead of sell to avoid giving up their low rates and to take advantage of a booming rental market.

In a finding highlighted in April’s Housing Wire magazine coverage of the report, the effects of interest rate lock-in are likely to be most acute in the strongest neighborhood housing markets because nearly half the 22 million Americans who refinanced while rates were at historic lows made 120% or more of their area’s median income and 44% lived in higher-income neighborhoods.

In recent years, the discussion of "lock in effects" has been focused on the millions of households unable to sell their homes because dramatic declines in property values meant they were underwater, or owed more on their mortgages than their homes were worth. IHS's report raises concerns that while rising house prices may potentially "unlock" underwater homeowners, allowing them to more freely sell their homes and buy new ones, they also may trigger a response from the Federal Reserve that may cause long term interest rates to increase will subsequently stall the recovery. While the IHS analysis focused on impacts going forward, coverage in the Washington Post raised concerns that interest rate lock in might already be having a dampening effect on home sales.

What we are working on next

In the coming months, IHS will be working to add even more to the ongoing conversation about the health of our local housing market, which we hope, in turn, sheds light some light on the national market as well. In the late spring, we will update the IHS Housing Market Indicators Data Portal with data for 2013. This update will include an accompanying web-only Housing Market Conditions Report that highlights our most recent findings from this new data and the relationships between the key indicators found on the Data Portal.

Later in the summer we will update key indicators from our Cook County State of Rental Housing report using the most recent data available and will take a deeper look at an issue impacting the availability of affordable housing both locally and nationally: the changing landscape of financing for smaller multifamily buildings – a key segment of Chicago's and many other cities’ affordable housing stock.

To be notified about new reports as well as new blog posts, and to give us feedback, follow us on Twitter, like us on Facebook, and join our LinkedIn Group.