The aftermath of the housing crisis has seen major institutional investors scooping up thousands of foreclosed or distressed homes in the Chicago region and throughout the country. Since 2012, HUD, Fannie Mae, and Freddie Mac have sold more than 130,000 troubled mortgages, the vast majority to private equity firms and hedge funds, according to a new report by the Center for Popular Democracy. In the last year alone, they find, Fannie Mae and Freddie Mac have sold 3,200 nonperforming loans to the highest bidder, all of which were Wall Street buyers, including a hedge fund by a former Lehman Brothers executive.

Given their often sizable investments in communities, the role of these investors in shaping the future of neighborhoods—either by acting as a stabilizing force or by pricing out former residents—remains an open question. Are the firms acquiring dilapidated properties, sprucing them up, and providing much needed rental housing? Will their competitive cash buying price out potential owner occupants? Or will they prove to be poor landlords whose renovated homes price out renters who could previously afford to live in a given neighborhood?

Institutional investors are often large Wall Street firms with only fleeting familiarity with the neighborhoods and cities they’re buying in, and their technology lets them purchase blocks of homes in a matter of minutes from the comfort of an office chair. In Chicago, institutional buyers tend to be most active in modest-income communities where prices have plummeted, distressed properties are available, and demand for rental housing is strong.

Last year, IHS looked at property sales records from 2013 to track where Blackstone, the largest institutional buyer in Cook County, had bought properties. In one striking case, Blackstone bought 111 single-family homes in Oak Lawn, a suburb in southwest Cook County where the median household income is slightly above the national median, at $57,000, and a typical home sells for $245,000, according to Zillow. Blackstone’s purchases accounted for 15.5 percent of all single-family sales in Oak Lawn. Blackstone was also very active in the Galewood neighborhood of the Chicago Community Area of Austin, in the southwest suburb of Oak Forest, and several other, mainly suburban, communities.

Large-scale institutional investors are a major subset of a broad and diverse group of distressed property investors whose activity, business models, and philosophies vary from market to market.

For example, the What Works Collaborative found that, broadly speaking, investors cycle through a variety of strategies depending on the conditions of the market. In Cleveland, for example, they focused almost exclusively on low-income neighborhoods, whereas in Las Vegas, they spread their purchases more widely. Allan Mallach has sorted buyers into four categories: a “flipper,” a predatory investor who buys homes and quickly sells them for more. The “milker,” who hangs on to properties for a brief period of time and rents them out for a quick profit. “Holders” rent properties for a longer term and invest more in their upkeep. According to the What Works study, depending on the city, investors renting out previously foreclosed properties reported cash-on-cash returns of 8 to 20 percent. Finally, the “rehabber” fixes up dilapidated properties and sells them for a sizable profit.

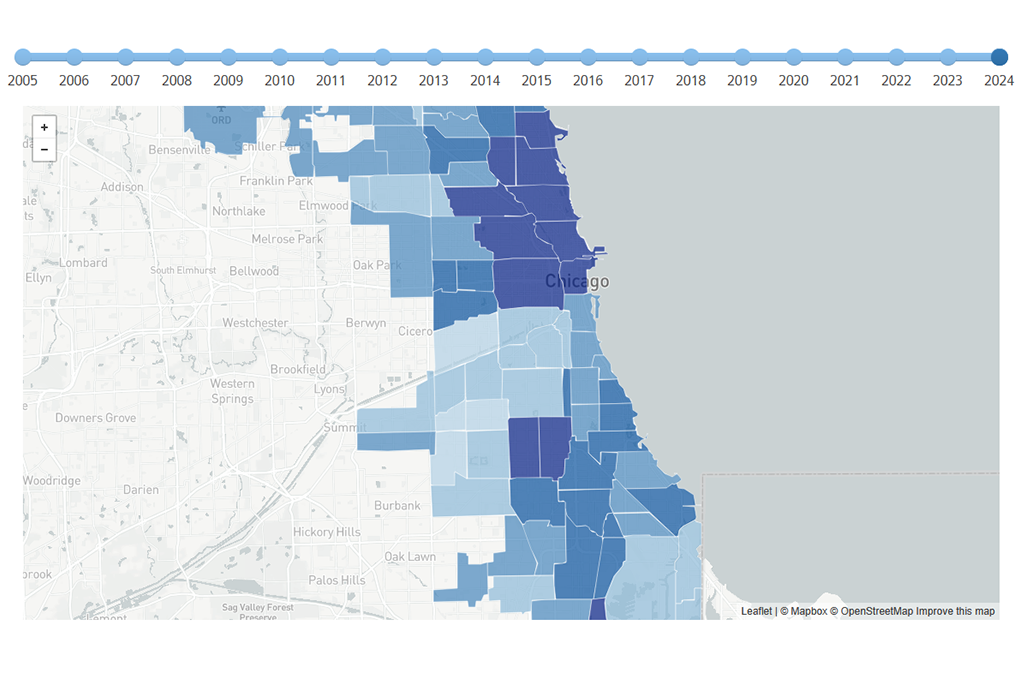

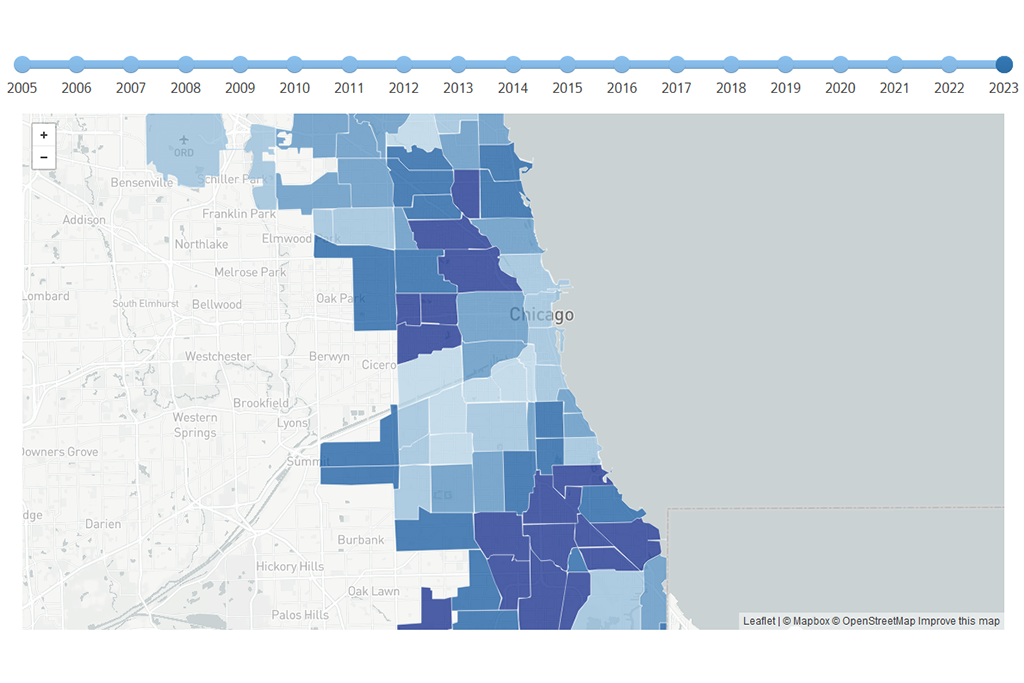

The IHS data reveal that together, all activity by business buyers, which include large institutional investors as well as smaller business entities buying single-family homes, peaked in 2013 for all counties in the Chicago region and declined in 2014. Business buyers accounted for 25 percent of all single-family sales in Oak Lawn in 2013 and 13 percent in 2014. In suburban Cook County communities such as Hazel Crest, Richton Park, Country Club Hills, Glenwood, Matteson, approximately 40 percent of all purchases were by business buyers in 2014.

Share of Single Family Homes Purchased by Business Buyers in the Chicago Six-County Region, 2005 to 2014

Share of Single Family Homes Purchased by Business Buyers in the Chicago Six-County Region, 2005 to 2014

In Chicago proper, business buyers have been particularly active on the South Side, although they’ve also begun to slow their purchases in 2014. More than half of the single-family home purchases in 2013 in Burnside South Chicago and Greater Grand Crossing were to business buyers, as were 45 percent in Auburn Gresham and Washington Heights.

Recent gains in home prices in the county and fewer foreclosures and distressed sales might be one reason for the recent declines in business buying. In fact, some large investors have begun to unload their inventories, but not always to owner-occupants. Recently, BLT Homes, another large business buyer in the Chicago region, announced that they were selling their national portfolio of properties, including many in Chicago, to another large investor, Cerebrus Capital Management.

RealtyTrac finds that most investors are hanging onto homes they’ve purchased, generating income from rents as they wait for prices to increase. The Joint Center for Housing Studies in its most recent State of the Nation’s Housing report finds that the 2010s are on pace to be the strongest decade for renter growth in history. Rents rose at a 3.2 percent rate last year in a very tight market. Given the sluggish housing rebound in several Chicago communities where investors have focused, that rental income may be appealing. As we’ve outlined in our recent report, home prices in Oak Forest and Oak Lawn, for example, are only up 10-14 percent from their bottom. Auburn-Gresham has bounced back only 15 percent.

What remains to be seen is the impact the investors will have on the character and demographic in the neighborhoods where they invested. Will they rehab homes and sell to a more affluent demographic, accelerating neighborhood change? Or will they help alleviate the rental housing shortage? More affordable rental housing is certainly needed, and investors in some cases have preferred to rent to low-income tenants with Housing Choice Vouchers because of the dependable rent and little turnover. Will these large investors prove to be good landlords and neighbors over the long haul or will tenants and municipalities struggle with poor property management and maintenance practices? A recent report by the California Reinvestment Coalition casts doubt on whether these large institutional buyers can be good neighbors. They find frequent instances of poor maintenance of rental units and other disinvestment in neighborhoods. The report by the Center for Popular Democracy calls out Blackstone in particular for imposing "unscrupulous terms" in its rental properties in Illinois, such as "as is" clauses, and for failing to maintain its rental portfolio. For now, though, the jury is still out.

Photo/Eric Allix Rogers