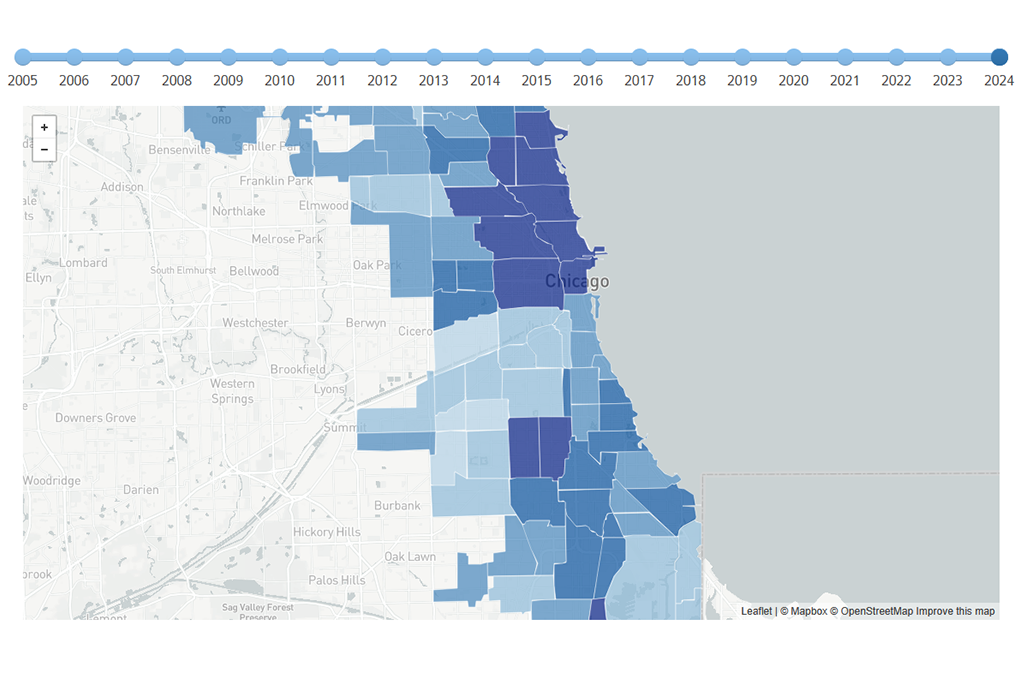

Homes in Chicago’s lakeside Lincoln Park neighborhood cost about what they did at the peak of the housing bubble that burst in 2006. But Lincoln Park, renowned for its luxury homes, is the exception in Chicago. According to our Cook County House Price Index, released today, home prices in the average Chicago neighborhood are still down 35 percent from peak levels. Although some neighborhoods have crept closer to their peak prices, the recovery has been uneven. Other neighborhood housing prices are down by more than half from their peak levels. View a full page interactive graph with a map and data for all submarkets here.

Chicago’s South and West sides have had the most difficult climbs toward recovery. Englewood and Greater Grand Crossing are 62 percent below their peak levels — the lowest in the city. It is not hard to imagine that a home purchased for $100,000 in 2006 might be worth just $38,000 today.

Lincoln Park and Lakeview are the only areas in Cook County where home values have returned to peak levels, with prices just 0.1 percent below their historic highs. The next strongest recovery is Lincoln Square and North Center, where prices are 3.4 percent below their peak.

The suburbs have also had a spotty recovery. In the affluent suburbs of Winnetka and Northbrook, homes are 10 percent below peak levels. But in Calumet City and Harvey, two far-south suburbs bordering Indiana, houses are 52 percent below their peaks.

Many peak home prices were inflated and unsustainable to begin with, so measuring recovery in terms of peak levels may seem to be too high of a bar. But for those who bought at the top of the market, that price point matters. When a mortgage is deep underwater, homeowners are essentially stuck in their homes unless they want to take a loss. Nationally, the percentage of homeowners with underwater mortgages was 16.9 percent in the fourth quarter of 2014, according to a recent Zillow report.

As the report stated, “negative equity is not an equal-opportunity predator.” Generally, houses that are less expensive, like those in Englewood or Calumet City, are more likely to be underwater than houses priced in the top one-third.

For example, Zillow’s analysis found that 26 percent of all Atlanta homes have negative equity, yet half are in the lowest tier of prices. While the tide may be changing for middle- and top-tier homes, bottom-tier areas in Chicago, Philadelphia, Detroit, and St. Louis and have seen an increase in the number of homeowners who are underwater, according to Zillow’s analysis.

The impact extends beyond the homeowners. With concentrated distress, entire neighborhoods struggle to regain their footing. Research has found that the greater the number of underwater mortgages, the higher the risk of neighborhoods spiraling into disorder. And, as a 2014 paper by the Federal Reserve Board described, the spillover effects of concentrated foreclosures in a neighborhood act in tandem. In the eyes of potential buyers, blighted properties reduce the value of neighboring homes and raise questions about the risks associated with buying. Meanwhile, the lower sale prices of foreclosed homes may affect the price of nearby homes if they’re being listed as comparable list prices. Completed foreclosures also increase the supply of for-sale homes. Together, the effects make it more difficult for families to regain equity and build stable wealth in their homes.

In Chicago and nationally, neighborhoods like Lincoln Park may have endured the housing crisis, but for others, a stable market with prices that allow homeowners to sell or regain equity is years away. The fallout from the collapse of 2006 will dog neighborhoods and communities for years to come.

Photo/Eric Allix Rogers