While the aging of the American population is one of the most critical demographic trends facing U.S cities, the Chicago region has limited data and analysis to inform current policy conversations around the housing needs of older adults.

The development of impactful policy to address the unique housing needs of Cook County’s older adults requires local and timely data on changing conditions, informed by the data needs of issue-area stakeholders. This analysis leverages the local knowledge of roughly 20 Chicago-area organizations working on older adult housing issues to create a practitioner-focused resource on key demographic and socioeconomic conditions related to older-adult housing demand and economic and housing insecurity in Cook County.

Intended as a baseline resource to inform current conversations and future analysis of critical housing issues facing older adults, Housing Needs and Economic Conditions of Cook County’s Older Adults establishes that households headed by an older adult represent a large and rapidly growing share of households in Cook County and that there is variation in both the current economic conditions and nature of older adult household growth in the city and suburbs. Critically, reflecting both the community and individual impact of systemic racial inequality and uneven economic opportunity for people of color, this analysis highlights that economic conditions such as income, cost burden, and presence of mortgage debt vary widely by older adult householder race and ethnicity and for older adults in the city and suburbs.

For information on data sources and methodology, click here. To access the data behind the figures in the report, click here.

BACKGROUND

The older adult population nationwide is growing at a faster rate than any other age group. It is projected that over the next two decades, a majority of growth in the number of households will be driven by seniors aged 65 and above. Despite this, not all communities are equipped for this significant demographic shift that will have future implications for housing.

Access to affordable, accessible, and stable housing is a key issue affecting older adults as they age. Before the COVID-19 pandemic, the number of housing cost-burdened older adults in the United States had reached an all-time high. While older adult renters are more likely to experience housing cost burdens compared to older adult homeowners, a growing share of older adult owners carry mortgage debt, and therefore additional housing costs, compared to previous decades. Among older adult renters and owners nationally, housing cost burdens were the most acute among very low-income older adults with annual incomes below $15,000. For older adults, housing cost burdens can influence their spending on essential medical care and other necessities, lowering their overall quality of life as their needs change. Income inequality among older adults has grown and has likely been exacerbated by the pandemic, with labor force projections anticipating a greater share of older adults delaying retirement throughout the next decade.

Nationally, older adults have the highest homeownership rates compared to any other age group, yet similar to the broader population, racial disparities persist. Black and Hispanic older adults have lower rates of homeownership than white older adults, and these gaps have grown since the Great Recession. Unequal access to homeownership can have implications for broader financial security into retirement years. Older adult homeowners’ housing costs can be significantly reduced at mortgage payoff. However, rising property taxes can be a financial strain among older adults with lower fixed incomes. During the pandemic, homeowners nationwide saw rising house price growth, possibly putting older adult homeowners in a favorable position to tap into their home equity as a source of retirement income if needed, but also potentially increased property tax burdens.

Not all older adults will be homeowners in their lifetime. Projections estimate that the number of older adult renters will reach an all-time high by 2040, with Black and Latino renters accounting for a bulk of this growth. Housing stability and affordability are a concern for older adult renter households, who experience greater cost burdens compared to the broader renter population and whose fixed incomes make it more difficult to deal with the potential of rising rents. During the pandemic, older adult renters were not immune to hardship, and a significant number of older adults faced possible eviction. With the number of older adults experiencing homelessness on the rise, affordable housing for older adult renters is a pressing concern as cities across the nation are seeing a declining supply of affordable rentals.

The disproportionate number of COVID-19 cases in institutional care settings during the height of the pandemic prompted greater public discourse on older adult housing needs, challenges, and living arrangements more generally. For example, the number of older adults living alone is projected to rapidly grow nationwide with implications for possible increased costs and decreased quality of life. Policymakers and housing providers are assessing if current programs and policies are adequate and tailored enough to meet the unique housing needs of older adults. A growing number of municipalities are looking beyond the home to proactively create age-friendly communities. While the COVID-19 pandemic’s long-term impacts on older adult housing needs remain unclear, the growing older adult population will impact the nature of housing demand and shape local housing markets for years to come.

Housing and Economic Conditions of Cook County’s Older Adults

To better address the housing needs of older adults and anticipate the impact of changes in older adult population on local housing markets, Cook County practitioners and policymakers need more information on the housing and economic challenges facing older adults today. Using data from the American Community Survey (ACS) 1-Year Public-Use Microdata Sample (PUMS), this report provides an analysis of current conditions in 2019, the most recent data available in 2021, and highlights how the composition of older adult households by income, race and ethnicity, tenure, and other indicators have changed in the City of Chicago and Suburban Cook County since 2012.1

This report shows that Cook County is aging, but that the nature of the growth in older adult households in the City of Chicago differs from Suburban Cook County. In Chicago, older adult households are increasingly renter households, with substantial growth in both Black and Hispanic older adult households and lower-income households. Additionally, older adult renter households in Chicago are increasingly living in 2 to 4 unit buildings, a critical but threatened component of the housing stock. In Suburban Cook County, where the aging of households is a central demographic characteristic, older adult households of color and very low-income Asian older adult households are growing most rapidly but still represent a small share of the older adult population, who is mostly white. In Suburban Cook County, older adults have fewer options for housing beyond single-family homes, and Black older adult households who own their homes have much higher rates of mortgage debt compared to their peers. These dynamics bolster concerns from local practitioners in both the City of Chicago and Suburban Cook County that existing public policy and the housing stock might not fully meet the needs of a substantial and growing older adult population and that the particular needs and challenges faced by lower-income and older adults of color more broadly may not be fully addressed.

KEY FINDINGS

Cook County is aging. Between 2012 and 2019, total households in Cook County increased by 49,613 households or 2.6 percent. Nearly all of this growth occurred in the City of Chicago, where households increased by 48,810 or 4.9 percent, while total households were relatively flat in Suburban Cook County. In Cook County, nearly 80,000 older adult households aged 65 and older were added between 2012 and 2019, a 19.4 percent increase. Figures 1 and 2 show household growth by age group in the City of Chicago and suburban Cook respectively. It shows that older adult households increased by nearly 45,000 households in the City of Chicago and by roughly 35,000 households in Suburban Cook County, or 24.2 and 15.4 percent, respectively.

A growing number of older adult households, amid modest or flat growth of total households, has led to an increased share of Cook County households headed by an older adult. Figure 3 shows that while 21.3 percent of households in Cook County were headed by an older adult in 2012, nearly a quarter of households were headed by an older adult by 2019. This “aging” of total households was most significant in Suburban Cook County, where an older adult headed 28.2 percent of households in 2019, up 3.7 percentage points from 2012. While this percentage point increase in older adult-headed households was similar in the City of Chicago in 2019, just 21.8 percent of households were older adult households in 2019, up from 18.4 percent of households in 2012.

Among older adult households, the number of households headed by a person of color is increasing fastest. Between 2012 and 2019, Figure 4 shows that countywide there was an 80.3 percent increase in the number of older-adult households that identify as Hispanic or Latino, a nearly 60 percent increase in Asian-identified older adult-headed households, and a 23.3 percent increase in older adult headed households that identify as Black or African American.2 This is compared to a 9.2 percent increase in the number of older adult-headed households that identify as white. In the City of Chicago, the largest percent increase in older adult households was seen in older adult households where the head of household identifies as Hispanic or Latino, which increased by 83.6 percent during this period.3

Generally, the growth in older-adult households of color is more rapid in Suburban Cook County, largely due to the overall smaller numbers of older adult households of color in the suburbs. Figure 5 illustrates the current composition of older adult-headed households by householder race and ethnicity as of 2019. It shows that despite growth in older adult households of color in Suburban Cook County, the vast majority of older adult-headed households in the suburbs identify as white.

As the older adult population becomes increasingly diverse, local decision-makers may need to examine how existing and new programs can remain inclusive and reach all segments of the older adult population. During stakeholder engagement, our partners noted the need to incorporate a racial equity lens in programs and policies, as well as the importance of culturally relevant materials and language translations to expand outreach to a diversifying older adult population.

In Chicago, older adult households are largely lower income. It is well documented that older adult households generally have lower incomes than households more broadly. According to the American Community Survey 5-Year estimates for 2019, the median household income for older adults in Cook County was $42,287 compared to $64,660 for all households. Similar to the broader population, there is substantial variation in the incomes of older adult households by race and ethnicity. Older adult households of color have lower incomes than white older adult households, generally.

Figure 6 illustrates the composition of older adult-headed households by race, ethnicity, and income in Chicago, and Figure 7 illustrates these same data for Suburban Cook County. Figure 6 shows that while 23.3 percent of white older adult households are very low income, far higher shares of Black, Hispanic, and Asian older adult households are very low income. Among all older adult households in the City of Chicago, 35.4 percent of households have incomes of less than 30 percent of Area Median Income (AMI) - or less than $22,614 in 2019. By comparison, just 17.3 percent of suburban Cook older adult households have incomes of less than 30 percent AMI but Black and Hispanic older adult households have much higher shares of very low income older adults than this suburban average and compared to white older adult households in particular. In 2019, Figure 7 illustrates that 24.5 and 22.3 percent of suburban Black and Hispanic older adult households were very low income compared to 15.4 and 20.9 percent of white and Asian older adult households, respectively.

Very large shares of low-income older adults are living on fixed incomes, often relying entirely on Social Security benefits. IHS partners reported that among the older populations they serve, these payments are often insufficient to fully cover necessities. As a consequence of low incomes, stakeholders reported high levels of food insecurity, particularly among very low-income older adult households earning below 30 percent of AMI.

The City of Chicago has seen an increase in very low-income Black and Hispanic older adult households while the Suburbs have seen a growing share of Asian older adult households with very low incomes. Figure 8 shows the percentage point change in the share of older adult households with very low incomes, earning less than 30 percent of the area median income. Between 2012 and 2019, the share of older adult white households that are very low income in the City of Chicago declined by 5.8 percentage points. At the same time, the share of older adult Black and Hispanic households that are very low-income grew by 5.6 and 6.7 percentage points, respectively. Among older adult Asian households, the share that earn lower incomes declined by 1.3 percentage points. During this same time period, the share of all older adult households that are very low-income increased by 1.4 percentage points citywide.

By comparison, Figure 9 illustrates these same data for Suburban Cook County and shows that the share of suburban older adult households that are very low income is declining. Between 2012 and 2019, the share of older adult households with incomes below 30 percent AMI declined by 2.3 percentage points. However, while the share of very low-income older adult white, African American, and Hispanic older adult households declined, the share of very low-income older adult Asian households grew by 8.2 percentage points. These trends add additional, local context to national data that highlights growing income inequality among older adult households and how this trend plays out by householder race and ethnicity in the city and suburbs.

In Chicago, most older adult households live alone – a trend that is driving growth in single households citywide. Figure 10 compares the share of older adult households that live alone across Cook County in 2012 and 2019 and shows that while this share grew in the City of Chicago it declined in Suburban Cook County. Figure 11 shows that the number of households living alone in Chicago increased by an additional 37,576 households since 2012, from roughly 374,000 households in 2012 to over 412,000 households in 2019. Over 70 percent of the total growth in single households in Chicago came from older adult households living alone which increased by 26,643 households during this period from roughly 96,000 older adult households in 2012 to nearly 123,000 in 2019.

Nationally, the occurrence of older adults living alone is expected to grow. Single-person older adult households are more likely to require assistance with mobility and care as they age, yet these households have lower median incomes and higher housing cost burdens. During stakeholder engagement, IHS partners reported a growing practice among senior housing providers of incorporating housing units for all ages and families in their developments. Stakeholders also expressed opportunities for policies to encourage multigenerational living arrangements as a way to both alleviate cost burdens and provide additional support for older adult needs as they age.

While older adult households primarily own their properties countywide, the share that rent their homes is growing rapidly in the city. As discussed above, most older adult households own their homes across the County; however, there is variation in the city and the suburbs. Figure 12 shows that roughly 83 percent of suburban older adults own their homes while just under 17 percent rent. By comparison, roughly 57 percent of older adult households own their homes in the City of Chicago while roughly 43 percent rent. Further, while the share of owner households is growing countywide, the share that rent in Chicago is growing substantially. Figure 13 shows that between 2012 and 2019, the number of older adult households that rent their homes increased by 44.1 percent while the number of older adult Chicago households that own increased by just 12.5 percent. By comparison, overall rental demand in the City of Chicago increased by just 4.4 percent and the number of owner households increased by 5.4 percent during this same period.

The growth in demand from older adult renter households in Chicago is anticipated to add pressure to the existing rental housing stock in the coming years. Among other issues, IHS partners noted the need for policies and programs to incentivize rental housing providers and property owners to incorporate accessibility features and repairs in the homes of older adult renters, who often have less control over their units compared to older adult homeowners and often have to pay for modifications without subsidy.

Roughly 60 percent of total older adult household growth in Chicago is from Black and Hispanic renter households. Figure 14 illustrates the relationship between the overall growth of older adult households and what these trends might mean for housing issues in Chicago, where a much larger share of older adult households rent. Data on these trends in Suburban Cook County are included in Figure 22, and other data for renter households in Suburban Cook are included in the report appendix.

The table below illustrates how older adult households by race and ethnicity and tenure contributed to overall increases in the City’s population of older adult households. It shows that increases in older adult renters accounted for nearly 68 percent of older adult household growth in Chicago between 2012 and 2019. It also shows that increases in Black and Hispanic older adult renters were the primary drivers of this trend. Between 2012 and 2019, 60.4 percent of the total growth in older adult households in the City of Chicago was from Black and Hispanic older adult renter households – 31.6 percent from Black identified older adult renter households and 28.7 percent from Hispanic identified older adult renter households.

As illustrated by Figure 15, this growth led to an increase in the share of older adult households of color that rent in the City of Chicago. As of 2019, the majority of Black and Hispanic older adult households rent their homes compared to 2012, when 44.4 and 37.1 percent of older adult Black and Hispanic households rented their homes, respectively. For Black and Hispanic older adult renter households, this translates to an increase of 14,191 and 12,866 households since 2012, respectively. By comparison, the share of white and Asian older adult households that rent was roughly unchanged between 2012 and 2019 although the number of households did increase slightly. Between 2012 and 2019, older adult white households that rent increased by 2,100 households, and Asian older adult households that rent increased by 1,334 households. Data on net change are included in the report appendix.

A large and growing share of Chicago’s older adult renter households have very low incomes. Figure 16 illustrates the composition of older adult renter households by income level in 2019. It shows that the majority of older adult households in Chicago are very low income and that roughly three-quarters of older adult renter households have incomes of less than 50 percent AMI. Further, Figure 17 below highlights that the number of lower-income older adult renters has grown substantially since 2012. It shows that the largest increase in older adult renters between 2012 and 2019 was among those earning less than 30 percent AMI which increased by over 13,300 households, or 33.3 percent. This was followed by older adult renters earning between 30 and 50 percent AMI, which increased by over 6,500 households, or 44.8 percent. Information on income ranges for 2012 and 2019 are included in the report methodology.

While the demand for and supply of affordable rental housing from lower-income households in Chicago has declined in recent years, the growth of older adult renter households with very low incomes points to an even greater need to proactively preserve and expand access to affordable rental housing, particularly units that accommodate the needs of older adults. For example, issue-area stakeholders interviewed by IHS expressed the importance of and need for increased housing subsidy to shield older adult renters with lower incomes from broader market pressures and rising housing costs.

In Chicago, most older adult renter households are cost-burdened and Black and Hispanic older adult renter households have the highest levels of cost-burden. In the City of Chicago, the data show that nearly 60 percent of older adult renters are cost-burdened, meaning that they pay more than 30 percent of their income toward rent. Figure 18 shows that most older adult renter households are cost-burdened at more substantial levels than renters are more generally – 58.7 percent of Chicago older adult renter households are cost-burdened compared to 47.4 percent of all Chicago renter households.

Additionally, the data show that cost burden is much more significant for Black and Hispanic older adult renter households than white or Asian older adult renter households. As of 2019, 71.4 percent of older adult Hispanic renter households, and 59.4 percent of older adult Black renter households were cost-burdened compared to 33.2 percent of older adult Asian4 and 52.9 percent of older adult white renter households.

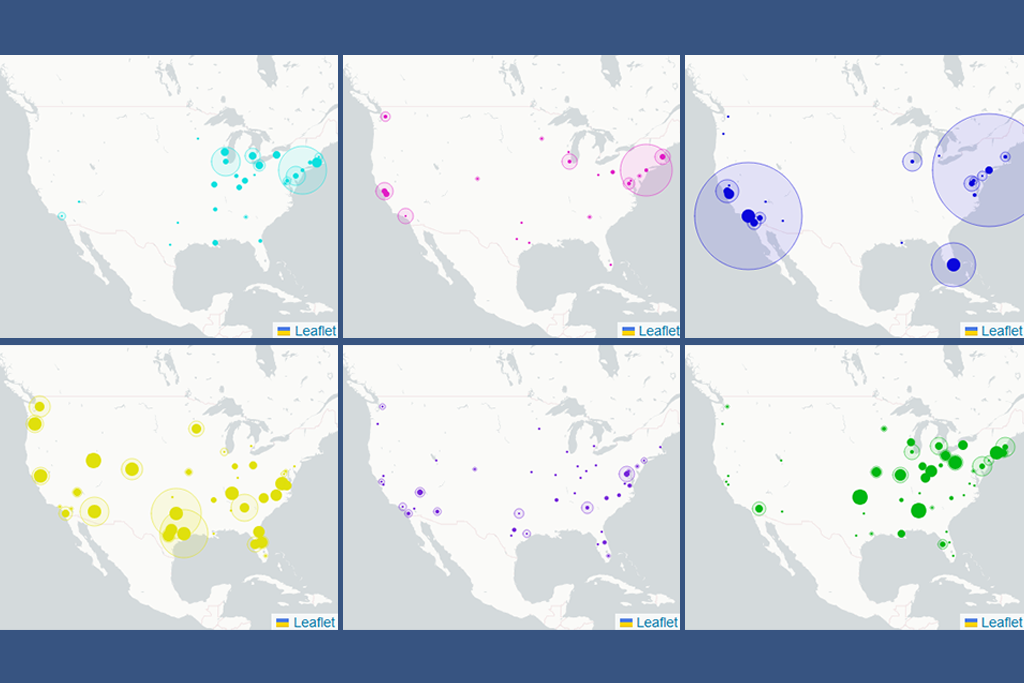

The largest growth in older adult renters is on Chicago’s Southwest and West Side neighborhoods. The interactive map below illustrates the net change in the number of older adult households that rent between 2012 and 2019 for 34 Cook County submarkets. It shows that the most substantial growth in older adult renter households was seen in Southwest and West Side Chicago submarkets including Austin/Belmont Cragin, Humboldt Park/Garfield Park, Bridgeport/Brighton Park, Gage Park/West Lawn, and Englewood/Greater Grand Crossing.

Submarkets that saw a decline in older adult renter households include City of Chicago communities in and around Uptown/Rogers Park, Portage Park/Jefferson Park, and Logan Square/Avondale. Many of these same areas are experiencing overall losses in the lower-cost rental supply and are losing lower-income renters. Many parts of Suburban Cook County also lost older adult renters including much of suburban South Cook County, communities around O’Hare Airport, and Winnetka/Northbrook.

To view a full-size map, click here. Underlying data for the map can be found in the report appendix here.

Figure 19. Net Change in Older Adult Households (65+) that Rent in Cook County by Submarket, 2012 to 2019

While most adult renters live in larger buildings, the share of older adults living in 2 to 4 unit buildings is increasing – counter to a trend seen among renters more generally. In 2019, the plurality of Chicago’s older adult renter households lived in rental units in larger buildings with 50 or more units. This share is declining, however. Figure 20 shows that whereas 42.5 percent of older adult renter households lived in these types of buildings in 2012, 37.1 percent of older adult renter households lived in these types of buildings by 2019 – a 5.4 percentage point decline. Instead, the city saw growth in the share of older adult renters living in 2 to 4 unit buildings from 26.5 percent of older adult renter households in 2012 to 31.8 percent by 2019 – a 5.3 percentage point increase.

Figure 21 illustrates that the city is seeing growth in older adult renter households in all building types, led by 2 to 4 unit buildings, which saw a net increase of 13,303 older adult renter households between 2012 and 2019. This represents a 73 percent increase in the number of older adult households that rent in 2 to 4 unit buildings. Conversely, the total number of Chicago renter households living in 2 to 4 unit buildings declined by 2.9 percent during this same period.5

IHS research has shown that 2 to 4 unit buildings make up a critical component of Chicago’s unsubsidized lower-cost housing stock, but these buildings are often older and owned by smaller, mom-and-pop landlords who may lack financial resources and incentives to make units in their properties “age-friendly” – or better able to adapt to changing older adult household mobility and quality of life needs. Additionally, stakeholders interviewed by IHS expressed that there are few existing incentives for landlords of 2 to 4s to incorporate accessibility modifications for older adult households and that resources for existing programs are inadequate to meet the current need.

In suburban Cook, 45.6 percent of total older adult household growth is from owner-occupied households that identify as white. Figure 22 illustrates how older adult households by race and ethnicity and tenure contributed to overall increases in the population of older adult households in Suburban Cook County. Data for the City of Chicago are included in Figure 14. The table below shows that increases in older adult owners accounted for nearly 90 percent of total older adult household growth in suburban Cook and that white households were the primary driver of this trend. Between 2012 and 2019, 45.6 percent of the total growth in older adult households in Suburban Cook County was from white older adult owner households. Notably, the second largest contributor to older adult household growth in the suburbs was from Black older adult owner households. In 2019, 17.1 percent of total suburban older adult household growth came from Black older adult owner households, this was 28.5 percentage points less than the share contributed by older adult white owner households, however.

The vast majority of suburban older adults own their homes and homeownership rates are high for all households regardless of the head of householder race or ethnicity. Figure 12 showed that in 2019, 56.9 percent of Chicago’s older adult households owned their homes compared to 83.2 percent of suburban older adult households. Figure 23 shows that in both the city and suburbs, the high homeownership share of older adults is driven by large shares of older adult owner households who identify as white. However, homeownership levels among older adults are high among all race and ethnic groups, particularly in the suburbs. Additionally, Figure 24 shows that the number of older adult households that own their homes increased across the county – growing fastest in Suburban Cook County and among white households.

Notably, the share of Black and Hispanic older adult households in the City of Chicago that own their homes declined below majority levels in 2019 while remaining flat for white and Asian older adult households. Through their counseling work, IHS partners reported that homeownership preservation is especially critical for Cook County’s Black and Hispanic older adults. These organizations reported that among the key challenges faced by their clients were unaffordable costs of insurance and property taxes that can contribute to elevated foreclosure risk as well as a need for succession and estate planning.

Despite high levels of homeownership among older adult households, there is substantial variation across the county in the composition of older adult homeowners by head of householder race and ethnicity. Figure 25 visualizes the share of older adult homeowners that are non-white in Cook County by submarket. The interactive map includes a tooltip that allows users to explore the race and ethnic composition of older adult homeowners in each submarket.

To view a full-size map, click here. Underlying data for the map can be found in the report appendix here.

Figure 25. Share of Older Adult Households (65+) Headed by a Person of Color by Submarket, 2019

Across Cook County, Black older adult homeowners are much more likely to have a mortgage than older adults that identify as white, Hispanic, or Asian. Figure 26 examines the share of older adult owner households who had a mortgage as of 2019 in the City of Chicago and Suburban Cook County by the head of householder’s race and ethnicity. It shows that in both 2012 and 2019 in Chicago and Suburban Cook County, owner households headed by a Black older adult had the highest shares of owners with a mortgage when compared to their peers of other races and ethnicities. In 2019 in Chicago, 47.7 percent of Black older adult owner households had a mortgage, compared to 43.3 percent of Hispanic or Latino older adult owner households, 33.8 percent of white older adult owner households, and 33.5 percent of older adult Asian6 owner households.

With the exception of white older adult owner households in Suburban Cook County, a larger share of suburban older adult households have a mortgage than their city counterparts - white suburban and white urban households have similar rates of owner households with a mortgage as of 2019. In Suburban Cook County, 62.4 percent of Black older adult owner households had a mortgage as of 2019 compared to 49.1 percent of Hispanic or Latino older adult owner households, 39.5 percent of Asian older adult owner households, and 33.2 percent of older adult owner households that identify as white. Notably, while the share of older adult households with a mortgage declined for every race and ethnic group in the City of Chicago between 2012 and 2019, the share grew for Black and white older adult households in Suburban Cook County during this same period.

For lower-income older adult owners, carrying mortgage debt into their retirement years may contribute to heightened housing insecurity. As older adult owners pay off their mortgage, housing costs can be significantly reduced. Stakeholders interviewed by IHS reported that in their homeownership counseling work, they have observed that their older adult clients in communities of color are more likely to start and pay off their mortgages later in life, impacting their ability to save and meet additional needs as they age. These partners also expressed that rising property taxes, property maintenance, unsustainable insurance, and utility costs can contribute to and compound existing housing cost burdens.

Most older adult homeowners across Cook County live in single-family homes, and this share is growing in Suburban Cook County. Figures 27 and 29 illustrate the share of older adult homeowners who live in single-family homes, 2 to 4 unit buildings, and larger likely-condominium units in buildings with 5 to 49 and 50 or more units in Suburban Cook County and the City of Chicago, respectively. These charts show that while most older adult homeowners live in single-family homes, housing options for older adults in the suburbs appear even more limited, reflecting the homogeneity of the housing stock in Suburban Cook County.

Figure 27 shows that in 2019, 81.8 percent of suburban older adult owner households lived in single-family homes, an increase of 0.4 percentage points from the share of older adult owners who lived in single-family homes in 2012. Conversely, the share of older adult owner households in the suburbs declined for all other building types during this period. Figure 28 shows the net change in older adult owner households in each building category and illustrates that despite a declining share of older adult owner households living in 2 to 4, 5 to 49, and 50 or more unit buildings during this period, the number of households in each building type grew. The declining share of households in other building types is due to the sheer size of the increase in older adult households in single-family homes experienced during this period – between 2012 and 2019 there was an increase of 27,504 older adult households living in single-family homes in Suburban Cook County. By comparison, Figures 29 and 30 show a declining share of older adult homeowners living in single-family homes in the City of Chicago, primarily due to the growth of older adult owner households living in other building types.

During stakeholder engagement, IHS partners raised concerns about the mismatch between Cook County’s existing housing stock for older adults and changing older adult housing needs and preferences. Specifically, that two-story single-family homes and multi-unit residential buildings that were built without accessibility features can limit older adults’ ability to age in place and remain in a community.

DISCUSSION AND NEXT STEPS

This analysis highlights the degree to which older adult households represent a large and growing share of households in Cook County. As a key demographic shift, this report demonstrates that addressing the housing needs of older adults is critical not only to the economic security of older adult households but also to the broader housing needs of the city and suburbs.

Housing Needs and Economic Conditions of Cook County’s Older Adults is intended as a baseline report to establish a collective understanding of conditions and broad housing challenges for older adults in Cook County. Understanding the nature of growth in the number of older adult households is essential for the development of impactful policy that addresses the housing security of older adults. This report complements the experience and recommendations of local stakeholders by showing that the nature of older adult household growth differs substantially among older adult households by race and ethnicity, income, tenure, and geography. Further, these findings emphasize that policy solutions must utilize a racial equity lens and address how housing security differs for owners and renters and among older adult households of different incomes in the city and suburbs.

As part of its mission, IHS will continue to engage its partners on the ground to build on this work by 1) continuing to provide technical assistance to Chicago region nonprofits working on older adult issues and 2) producing new analysis highlighting legacy and emerging issues impacting the housing security of older adults in Cook County to advance policy change. For example, this report highlights that, among other issues, additional practitioner-focused and practitioner-engaged research is needed to better understand the implications for growth in single older adult households in Chicago and the need for housing options that support multigenerational households; the levels and types of mortgage debt carried by older adult homeowners, particularly Black older adult owners who are more likely to have a mortgage than their peers; and the suitability, sustainability, and affordability of the housing stock in serving older adults as they age.

To keep up-to-date on IHS analysis, sign up for our email list, follow us on Twitter, Facebook, or LinkedIn.

This project was funded with generous support from the RRF Foundation for Aging. IHS would like to thank the many individuals and organizations who shared their issue area expertise throughout the development of this report. Many of these insights are shared in the companion blog to this report, Planning for the Housing Needs of an Aging Population.

1. Because this analysis focuses on economic conditions of older adults, this report focuses on households, not population. As such, this analysis uses the age and stated race and ethnicity of the head of household to identify both older adult households defined as households headed by a person 65 or older and older adult households by race and ethnicity. Additionally, because this analysis is focused on households, the analysis excludes older adults who live in skilled nursing facilities and in assisted living facilities where occupants are not reported as individual households. According to the American Community Survey, older adults living in these types of living situations are classified under Group Quarters and, as such, key data used in this analysis such as income, race and ethnicity, cost burden, and tenure are not reported.

2. Head of householder race and ethnicity is categorized as follows from the American Community Survey. A white person is a person who identified as white alone; a Black or African American person is a person who identified as Black or African American alone; a Hispanic or Latino person is a person who identified as Spanish/Hispanic/Latino origin; an Asian person is a person who identified as Asian alone; and a person categorized as All Other Race/Ethnicity Head of Householder is a person who identified as American Indian or Alaska Native or Native Hawaiian and Other Pacific Islander or Some Other Race or Two or More Races.

3. Future references to head of householder race and ethnicity will be simplified and generalized to refer to the household only. A household where the head of household identifies as white is referred to as ‘white’; a household where the head of household identifies as Black or African American is referred to as ‘Black’; a household where the head of household identifies as Hispanic or Latino is referred to as ‘Hispanic’; and a household where the head of household identifies as Asian is referred to as ‘Asian’.

4. According to IHS calculations for 90% confidence level margins of error (MOE), cost-burdened renter older adult households with a head of household who identifies as Asian has a high MOE. This result should be interpreted with caution.

5. Figures for overall declines in renter households living in 2 to 4 unit buildings reported in this analysis differ from declines reported in IHS’s 2021 State of Rental Housing in Cook County report. This analysis examines changes in occupied rental units, while the State of Rental highlights shifts in the total stock, which includes both occupied and vacant rental units.

6. According to IHS calculations for 90% confidence level margins of error (MOE), older adult owner households with a mortgage with a head of household who identifies as Asian has a high MOE. This result should be interpreted with caution.