The newest release of the State of Rental Housing in Cook County updates key data on changing rental demand, the supply of rental housing, and how these dynamics affect access to affordable rental housing for Cook County's lowest income households. The report also includes an in-depth, submarket-level analysis examining changes in the affordable rental housing supply and its implications for lower-income renters, and how these changes vary across the City of Chicago. Summary data for Cook County, the City of Chicago, and suburban Cook County are featured in the data appendix.

While this analysis does not include data covering the COVID-19 pandemic period, the report uses the most recent data available from the American Community Survey through 2019, and data used in this report can serve as a valuable tool to guide policy discussions and inform strategies during the post-COVID recovery period. This analysis focuses on how conditions have evolved throughout the Great Recession recovery period from 2012 through 2019 and provides an important baseline for understanding housing needs and conditions that have been exacerbated by the COVID-19 economy.

For information on data sources and methodology, click here. To access the data behind the figures in the report, click here.

BACKGROUND

At the onset of the pandemic, the national unemployment rate surged from a record low in February 2020 to the highest rate since the Great Depression by May 2020. In response, Congress negotiated several rounds of stimulus aid packages to keep pace with growing need from individuals and families in financial distress. Lawmakers and practitioners developed policies and programs to stabilize vulnerable residents and distribute emergency financial assistance. At the same time, public agencies and community organizations distributing emergency aid navigated challenges as they emerged.

More than a year into the COVID-19 pandemic, the national economy is showing signs of recovery. However, the pandemic’s economic impacts remain uneven. At the start of the COVID-19 recession, initial job losses hit low-income individuals and families the hardest. Even as the broader economy gradually improves, unemployment remains significantly higher among low-income workers nationwide while middle- and higher-income workers have met or exceeded pre-pandemic employment levels. Additionally, while the country has experienced economic recovery in recent months, new cycles of the pandemic add additional uncertainty to projections of future economic growth.

As economic and housing market conditions slowly improve, existing data can help guide equitable recovery efforts. The vast surge in economic hardship seen within weeks of initial shutdown orders led many affordable housing advocates to anticipate an eviction crisis similar to the wave of foreclosures seen during the Great Recession. While the worst outcomes have yet been avoided, vulnerable renter households hit hardest will likely experience a longer and slower recovery. It is likely that the economic and rental housing challenges that pre-date the crisis will continue to persist as communities return to pre-pandemic conditions. Since some of these ongoing challenges were exacerbated by the COVID-19 recession, existing and historical data on rental housing trends can assist policymakers and practitioners in targeting programs that stabilize renters at risk of displacement once temporary policies expire and developing longer-term solutions that expand access to affordable housing through a range of strategies and policy interventions.

TRENDS IN PRE-PANDEMIC RENTAL DEMAND IN COOK COUNTY

Understanding demographic and economic characteristics and shifts of Cook County’s renter households can help practitioners and policymakers better understand the region’s changing rental demand, evaluate existing needs to prioritize resources, and develop targeted strategies to stabilize vulnerable households during the post-COVID recovery period.

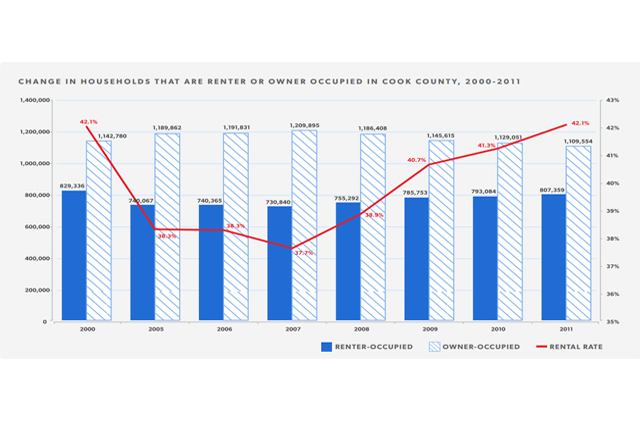

Cook County’s rental rate leveled off from peak levels seen in 2015 but remains historically high

As noted in previous State of Rental Housing in Cook County reports the share of Cook County households that rent increased substantially after the housing market crash in 2007 and remained high during the recovery period after 2012. After reaching peak levels in 2015, when 44.2 percent of all Cook County households were renters, the rental rate has steadily declined and remained at a steady rate of around 43 percent within the last few years. In 2019, nearly 857,000 households in Cook County rented their homes or 43.2 percent of all households.

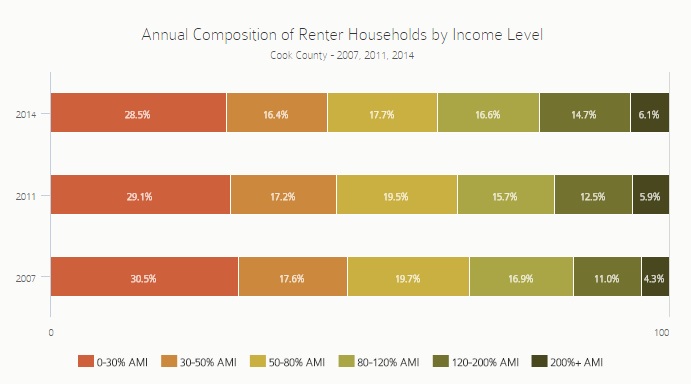

Partly due to a loss of very low-income renter households, Cook County’s renter household composition continues to shift towards households with higher incomes

Cook County continues to see a loss of very low-income renters. Previous State of Rental Housing in Cook County reports have documented that despite remaining the largest group of renter households by income in Cook County, the county is losing very low-income renters earning below 30 percent of the area median income (AMI). In 2019, 26.6 percent of all renters in Cook County were very low income compared to 30.7 percent of all renters in 2012. From 2012 to 2019, low-income households earning 30 percent AMI and below decreased in Cook County by 26,579 households, a 10.4 percent drop, the largest of any other income group.

While the decline of very low-income households may be attributed to rising incomes, given long-term trends in wage stagnation, it is more likely these households have left the region due to affordability pressures, including rising rents or disinvestment-related factors. In Chicago, very low-income households have declined across all market types, with the largest losses in high-cost areas. On the other hand, lower-cost communities in Chicago that are home to a higher share of low-income households are experiencing population losses across all income groups.

At the same time, the share of renter households earning between 30 and 50 percent AMI grew, as did the share of middle- and higher-income renter households. Although higher-income households remain a relatively small share of all renters, households earning more than 120 percent AMI are becoming a larger share of total renter households. Neighborhoods that see substantial growth in rental demand from higher-income households may experience growing pressures on their unsubsidized affordable housing stock and growing displacement risk among lower-income renter households.

For lower-income households, unemployment during the COVID-19 pandemic exacerbated preexisting housing insecurity, and these households are at risk of further destabilization. Nationally and in Illinois, a large majority of renter households struggling to pay rent during the pandemic are low-income and at increased risk of eviction. Data above documenting the changing composition of renter households illustrate that low-income households were already facing affordability pressures before the pandemic.

While national and state eviction moratoriums have stabilized at-risk renter households, many renters will continue to face rent arrears after these moratoria expire. As states and localities distribute emergency rental assistance to renters and property owners, sustained protective policies, economic supports, and longer-term solutions may be needed until all segments of the job market recover and vulnerable households gain a better financial footing.

Growth in renter demand since 2012 has been driven by households headed by older adults

Due to the aging of the overall population in Cook County and nationwide, the share of older adult renters is on the rise. In Cook County, renter household growth is concentrated among older householders, particularly for renters aged 65 to 74. From 2012 to 2019, every renter household age group in Cook County declined or remained stagnant except for households aged 55 and over. Whereas all renter households grew by 3.4 percent, households headed by a person aged 55 to 64 and 65 to 74 increased by 12.7 percent and 45.2 percent, respectively. During this same period, households headed by a person aged 75 and above increased by 15.9 percent.

Despite the growth in older adult renters, younger renter households headed by a person aged 25 to 34 continue to comprise the largest share of total renter households. Previous State of Rental reports documented that rental demand during the Great Recession and recovery period was driven by growth in younger renter households, reaching a peak in 2014. Since then, this age group's share has declined and remained stable. Roughly 30 percent of all renter households in Cook County are headed by a person between the age of 25 and 34.

The public health impacts of the COVID-19 pandemic calls greater attention to the housing conditions and needs of older adult renter households. During the height of the pandemic, occupancy rates in institutional settings such as nursing homes and assisted living facilities sharply declined. Although this change may not be permanent, the pandemic has prompted communities to consider how policies and programs can better accommodate the housing needs of older adults as they become a rapidly growing share of the overall population.

The projected growth of older adult renters will likely continue to outpace other age groups and will have impacts on local housing markets beyond the pandemic. Older adult renter households may face unique challenges, such as housing affordability on fixed incomes. Communities must develop holistic strategies and solutions to address this age group’s unique housing needs and mitigate growing housing affordability challenges.

TRENDS IN PRE-PANDEMIC RENTAL SUPPLY IN COOK COUNTY

Pre-pandemic data trends on Cook County’s changing rental supply can inform targeted solutions to close the region’s longstanding affordable housing shortage. Contextualizing the ways that pandemic-related housing challenges compound existing longer-term affordability trends can inform policy development and program design during the recovery period.

Cook County continued to see losses in its small and mid-sized rental stock while additions to the rental supply were concentrated in larger buildings

Cook County has seen substantial growth in the rental stock in buildings with 50 or more units and modest growth in single-family homes. In Cook County, rental units in large buildings with 50 or more units have experienced the largest growth of any building type. From 2012 to 2019, rental units in 50+ unit buildings have increased by 15.3 percent or 26,898 units. In the City of Chicago, buildings with 50 or more units were the only type of structure to have seen growth in the number of rental units. While the number of single-family rentals has seen modest growth in Suburban Cook County since 2012, it has leveled off after its peak in 2015.

At the same time, Cook County also experienced losses in its small- and mid-sized building stock. In the City of Chicago and Suburban Cook County, rental units in 2 to 4 unit buildings continue to see the largest losses, followed by units in 5 to 49 unit buildings. Previous State of Rental Housing in Cook County reports and other IHS research have documented the importance of and threats to the County’s stock of 2 to 4 unit buildings.

Whereas the number of rental units in 2 to 4 unit buildings has grown in recent years as vacant or formerly owner-occupied units became occupied as rentals or as some single-family homes were converted to small rental buildings in areas with lower demand for homeownership, the result is still a significant net loss of 7 percent of the 2 to 4 stock or 20,701 units since 2012. Units in 2 to 4 unit buildings represented 33.2 percent of the county’s rental stock in 2012, but these buildings represented 30.7 percent of the stock in 2019.

Much of Cook County’s unsubsidized affordable rental stock is located in small and mid-sized rental buildings, yet this stock faces continued risk of turnover and loss during the COVID-19 pandemic. This stock of lower-cost rentals experienced sustained losses during the Great Recession and recovery period despite overall growth in Cook County’s rental supply.

Two to 4 unit buildings remain particularly vulnerable. These smaller residential buildings often support greater affordability and house higher shares of lower-income tenants vulnerable to COVID-19 unemployment. Nationally, small rentals have experienced higher rates of nonpayment during the pandemic. At the same time, property owners of these small rentals often have fewer financial resources and capacity to weather sustained rent shortfalls or tap into emergency rental assistance programs without potentially falling into foreclosure or experiencing heightened pressures to sell. During the COVID-19 pandemic and recovery period, units in small and mid-sized rentals across all markets require targeted preservation strategies in order to close the County’s affordable housing shortage.

TRENDS IN PRE-PANDEMIC RENTAL AFFORDABILITY IN COOK COUNTY

Pre-pandemic data trends for Cook County’s rental housing affordability can serve as a baseline that measures the scope of need as practitioners and policymakers continue to distribute emergency rental assistance and protect vulnerable renters from eviction. These data below can also inform how different demand- and supply-side policies and strategies can close the region’s longstanding affordability gap and reduce housing cost burdens during the recovery period.

In every State of Rental Housing in Cook County report, IHS documents the mismatch between the number of households in Cook County that need affordable rental housing and the number of units that are affordable. This “affordability gap” is defined as the difference between the demand for rental housing by lower-income households earning 150 percent of poverty, or $39,258 annually, and the supply of units that would be affordable at 30 percent of a lower-income household’s income—about $981 per month. Affordable demand also includes renter households earning more than 150 percent of the poverty level but who live in units that are affordable to lower-income households.

The affordability gap is useful as a broad indicator to highlight the mismatch between the supply of and demand for affordable rental housing countywide and documents the scope of pre-pandemic affordable housing need. However, the affordability gap does not necessarily directly translate to the number of units that need to be built to solve the region’s affordability challenges. Rather, a range of policy interventions are needed to address this issue. While some lower-income renters experience a slower recovery, policies that expand and preserve the supply of affordable housing and demand-side subsidies to stabilize renters experiencing prolonged unemployment from the COVID-19 recession can narrow the affordability gap. These strategies may include, but are not limited to, increased access to voucher-based subsidy, new construction of affordable units in stronger markets, and different innovative solutions to preserving existing affordable units in neighborhoods with a shrinking affordable supply.

Losses in the number of lower-income households are behind a shrinking affordability gap while affordable supply remains stagnant

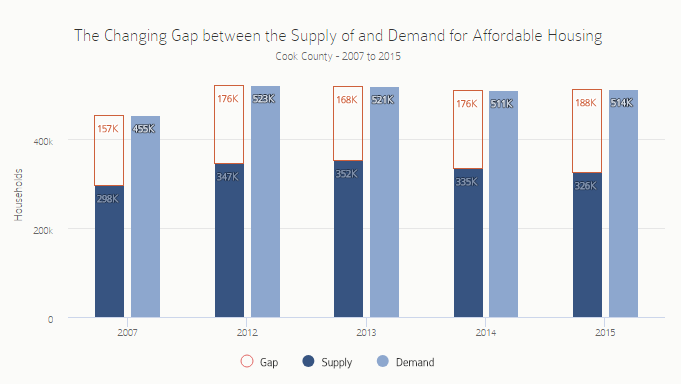

Cook County’s affordability gap has narrowed but the county still faces a large shortage of affordable housing. Since 2012, the County’s affordability gap decreased by 9.7 percent, or 17,091 units, due to the number of lower-income households earning 150 percent of the poverty level declining at a faster rate than the supply of affordable rentals. This marks an improvement from 2015 when the county lacked the largest number of affordable units relative to demand from lower-income households - at 187,848 affordable units. However, this represents a small dent in the county’s affordable housing shortage, which stood at 159,122 units in 2019.

The slight improvement of the affordability gap can be attributed to losses of lower-income households in the County. Previous State of Rental reports illustrate that the number of lower-income households in Cook County has been on a steady decline since 2015. Indexed to 2012, affordable supply and demand in 2019 both declined at roughly the same rate of 10.2 and 10 percent, respectively. However, the affordable supply would need to increase at a rate far greater than changes in lower-income households to close the affordability gap, which stood at 176,213 units in 2012. Fewer households demanding affordable units may signal households leaving the City from growing affordability pressures rather than these households attaining upward economic mobility.

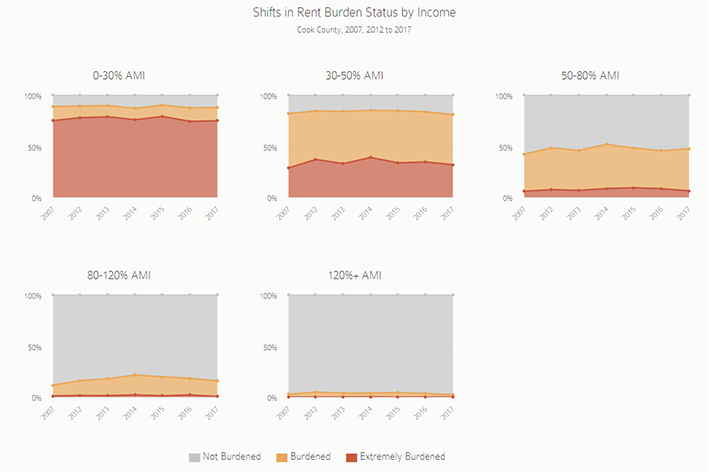

Despite declines in housing cost burden countywide, unaffordability remains high among very-low and low-income households

Concurrent with a declining affordability gap, the number of cost-burdened renter households declined for all income groups except households earning between 30 and 50 percent AMI. Between 2012 and 2019, 7,627 additional households earning 30 to 50 percent AMI were cost-burdened, or paid in excess of 30 percent of their incomes towards rent, while the number of cost-burdened households decreased for other income groups. The group with the largest decline in cost burden are renter households earning below 30 percent AMI - from 2012 to 2019, the number of these cost-burdened renter households fell by 29,156. Changes in the number of these low-income cost-burdened households also coincide with broader household-level changes countywide. Countywide, the population of households earning less than 30 percent AMI declined by 26,579 households after 2012. Despite these declines, nearly 87 percent of renter households earning less than 30 percent AMI face housing cost burdens.

KEY TRENDS IMPACTING AFFORDABILITY IN THE CITY OF CHICAGO

Pre-pandemic data below on changing affordability levels in Chicago can help city leaders prioritize affordable housing investments, develop tailored strategies and solutions to meet affordability challenges in different submarkets, and deploy pandemic aid to mitigate existing displacement pressures faced by lower-income renters. These strategies may include maintaining and investing in existing affordable rental housing in communities where it exists and expanding access to neighborhoods where affordable rentals are vulnerable to market pressures.

This section examines the nature of changing affordability in the City of Chicago and submarkets where renters are likely facing greater affordability pressures. This section highlights the longer-term decline in the affordable supply since 2012, how this has impacted lower-income households, and how these dynamics play out in certain submarkets across the City.

Long-term losses outpace recent additions to the affordable supply

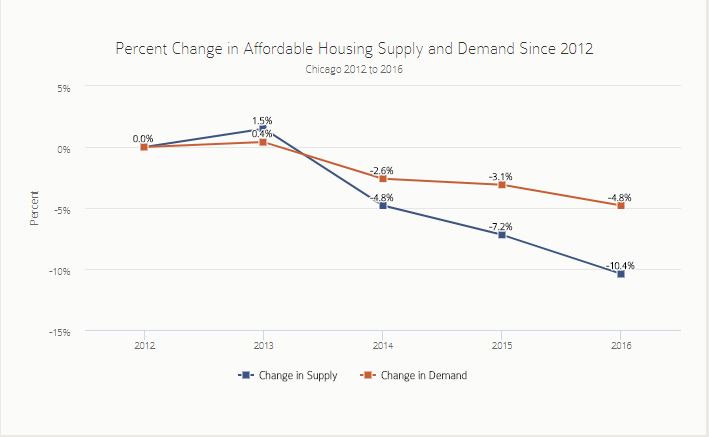

The chart below shows the longer-term changes in the supply of affordable rental units relative to demand in the City of Chicago indexed to values in 2012. Previous State of Rental Housing in Cook County reports documented that the supply of affordable rental units in Chicago was declining at a faster pace than demand from lower-income households, contributing to a growing affordability gap. While this year’s update illustrates that the supply of and demand for affordable housing are both declining at a similar pace, demand for affordable housing has consistently outnumbered the availability of affordable housing, even as lower-income households continue to leave the City.

From 2012 to 2019, Chicago has roughly 24,000 fewer available affordable rentals representing a 9.5 percent decline in the affordable supply, even accounting for the modest expansion of affordable units in recent years. Due to continued long-term declines, the affordable supply would need to grow at a faster rate to meet existing demand from lower-income households. In 2019, the city faces a gap of 100,197 affordable units, slightly less than the gap of 110,639 units observed in 2012.

The affordability gap is useful as a broad indicator to highlight the mismatch between the supply of and demand for affordable rental housing countywide and documents the scope of pre-pandemic affordable housing need. However, as noted earlier, the affordability gap does not necessarily directly translate to the number of units that need to be built to solve the region’s affordability challenges. Rather, a range of policy interventions are needed to address this issue.

Submarkets on Chicago’s north and northwest side continue to see the largest declines in affordability

Approximately 40 percent of the rental units in Chicago are affordable for lower-income households earning 150 percent of the poverty level. However, different submarkets in the City of Chicago encompass a wide range of affordability levels for lower-income households, and some have seen recent steep declines in the availability of affordable rentals.

Similar to previous State of Rental reports, a handful of submarkets on Chicago’s north and northwest side saw the largest longer-term losses in affordability. Affordable rental housing can be lost either through rent increasing to unaffordable levels, conversion to higher-cost or non-rental housing, or deterioration. Averaging the share of affordable rentals from 2012-2014 to 2017-2019, the City of Chicago experienced a 5.2 percentage point decline in affordable rental units. Certain Chicago submarkets recorded an even greater decline in the share of affordable rentals, however. For example, Logan Square/Avondale, Portage Park/Jefferson Park, West Town/Near West Side, and Lincoln Square/North Center saw declines in affordable rental units by 14.4, 12.3, 11.3, 11.3 percentage points, respectively.

Submarkets with the lowest levels of affordability also have some of the highest shares of lower-income households in high-cost units and include the Loop, Lake View/Lincoln Park, Lincoln Square/North Center, West Town/Near West Side, and Logan Square/Avondale. These high-cost submarkets have likely lost formerly affordable rentals to market pressures through rent increases and conversions to more expensive housing types such as condominiums and single-family homes.

The map below illustrates the change of affordable units averaged between 2012-2014 and 2017-2019 across 17 Chicago submarkets. A three-year average was created to account for small annual sample sizes at the submarket level. More information on the methodology for calculating three-year averages can be found here. Data for submarkets can be found in the appendix.

The chart and interactive table below examine the shifting dynamics of IHS’s affordability calculation for the City of Chicago and for 17 Chicago submarkets. The chart breaks out changes in 1) the share of occupied rental units that are affordable to lower-income households earning 150 percent of poverty, 2) the share of renters that are lower-income, and 3) the share of lower-income renters living in unaffordable units between 2012-2014 and 2017-2019. The interactive table includes these same data at the submarket level, as well as data on current conditions in 2017-2019.

Between 2012-2014 and 2017-2019, the City of Chicago saw declines in both its share of rental units that are affordable and share of renter households that are lower-income. The share of the rental supply that is affordable experienced a larger percentage point decline than the share of renters that are lower-income - the affordable supply declined by 5.2 percentage points while the share of renters that are lower-income declined by 4.2 percentage points. Additionally, the share of lower-income renters that face greater housing insecurity has grown. The share of lower-income renters in unaffordable rentals has increased by 2.4 percentage points since 2012.

The interactive table below shows how the relationship between declining affordability, the loss of lower-income renters, and increasing affordability pressure on remaining lower-income renters plays out in submarkets across the city. Between 2012-2014 and 2017-2019, 13 of 17 submarkets in the city saw declines in the share of rental units considered affordable. Nearly all of the submarkets with a declining share of affordable rental units also saw losses in their population of lower-income renter households. This trend was particularly stark in submarkets on the north and northwest side that saw the largest declines in affordable supply. For example, lower-income renter households in Logan Square/Avondale and West Town/Near West Side declined by 16.5 and 11 percentage points, respectively.

For lower-income renters that continue to live in the city, a growing share are facing greater affordability pressures in 12 Chicago submarkets. Between 2012-2014 and 2017-2019, Irving Park/Albany Park, Lincoln Square/North Center, the Loop, and Portage Park/Jefferson Park saw the largest growth in shares of lower-income renters living in unaffordable units. The share of lower-income renters in unaffordable units increased in these submarkets by 11.8, 11.5, 10.7, and 9.1 percentage points, respectively.